Lesson 4 - Time Value of Money

|

|

This lecture teaches financial analysts the time value of money. The lecture starts with the present value of a single future payment and evolves into the present value of multiple future withdrawals and payments. Finally, an amortization table is constructed for fixed payment mortgage.

|

Single Investment

|

|

1.

The Present Value Formula

places a value of future cash flows in terms of money today.

- Emphasizes the present

- For example, I deposit $100 into a bank at 5% interest rate.

- After one year, I earn 0.05($100) = $5 in interest. My balance is $105.00

- After two years, I earn 0.05($105.00) = $5.25. My balance is $110.25

If let the money earn interest after n years, then I can build the sequence

In one-hundred years, $100 grows into $13,150.13 at 5% interest.

- Notation

- FV is Future Value

- PV is Present Value

- n or t refer to the time

- i is the discount rate or interest rate

- subscripts refer to time

2. Present value - rearrange equation and solve for PV 0

- One hundred years is very far away.

- I rather have the money today.

- The present value of $13,150.13 in one hundred years is worth $100 to today.

- I can take that $100 today, invest it in a savings account with 5% interest, and let it grow to $13,150.13

If I receive a payment in the future, then the present value is:

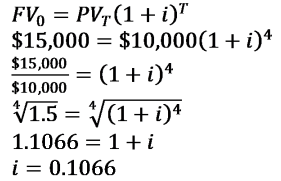

3. Solving for the interest rate

- Example

- You have $10,000 to invest

- You want to earn $15,000

- You want your money in 4 years

- What is the minimum interest rate you need to earn?

- You need to earn at least 10.66% interest to meet your goals

4. The

Rule of 72

- an easy way to determine how long it takes something to double in size

The Equation

- Examples

- Bank Account

- If your bank deposit is earning 4% per year, divide 72 by 4, and your bank account will double in 18 years

- If your bank deposit is earning 7% per year, divide 72 by 7, and your bank account will double in 10.3 years

- If you plan to put money into a savings account for 5 years, divide 72 by 5, and your interest needs to be 14.4% to double

- Economic Growth

- China's economy is growing 10% per year; divide 72 by 10, which means China's economy will double every 7.2 years

- U.S.A. is growing 1% per year, divide 70 by 1 and the U.S. economy will double in 70 years

|

Multiple Investments

|

1. Let’s change the analysis, so we receive multiple future payments.

- Every year, I invest $500 into the bank account at 6% interest.

- After the first year, I earn $500(0.06) = $30 My balance is $500 + $30 + $500 = $1,030

- After the second year, I earn $1,030( 0.06 ) = $61.80. My balance is $1,030 + $61.80 + $500 = $1,591.80

- After the third year, I earn $1,591.80(0.06) = $95.508. My balance is $1,591.80 + $95.508 + $500 = $2,187.308

- If I wrote an equation

- How much is it worth to me today, if I receive $500 today, $500 in one year, $500 in two years, and $500 in three years?

- If I received $1,836.51 today, I can invest in a savings account and earn $2,187.31 in three years. (Rounding error)

2. Uneven withdrawals and investments

- This formula is flexible.

- I can withdraw or invest any amounts.

- If the interest rate is 14% and investment time is four years

- For example

| Year |

Activity |

Amount |

Interest + Balance |

| 0 |

Deposit |

$100 |

$148.15 |

| 1 |

Deposit |

$300 |

$389.88 |

| 2 |

Withdrew |

$50 |

-$57 |

| 2 |

Deposit |

$100 |

$114.00 |

| 3 |

Withdrew |

$75 |

-$75

|

|

|

Total

|

$520.03

|

- How much are these cash flows worth to me today if interest rate is 14%?

- If I invest $351.01 today at 14% interest, then in 3 years, I will have $520.04.

|

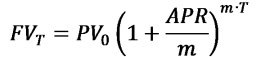

Compounding Frequency

|

1. Interest rates are defined as Annual Percentage Rate (APR)

- For example, is 1% a good interest rate for a borrower?

- There is no time units.

- If 1% is annual, then it is a good rate.

- If it is daily, then the rate is terrible.

- The borrower borrowed money from a loan shark.

- All interest rates are defined in annual terms, unless otherwise stated.

- Usually loan payments and bank interests are calculated monthly.

- Loans could be semi-annually (two payments per year)

- Loans coudl be quarterly (four payments per year).

Adjust the equation as follows

- m is compounding

- Example

- You put $10 in your bank account for 20 years

- Earns 8% interest (APR)

- Compounded monthly

- Your savings grow into:

Note: if this was compounded annually, then it would be $46.61

2.

Effective Annual Rate (EFF)

- the equivalent interest rate if the compounding were once a year.

- Example: Convert the interest rate 8% APR compounded monthly into an interest that is compounded annnually

- Example: If you put $10 in your bank account for 20 years that earn 8.3% APR compounding yearly, then your savings grow into:

3. Present and future value problems with multiple cash flows can be compounded monthly, semi-annually, or quarterly.

- Example

- What is the present value if I receive $50 within a month, $100 within six months, $75 in exactly one year and one month, and the interest rate is 10%.

- The smallest time unit is the month, so we need to adjust the time units for interest percent and time.

- Time is monthly

- Interest rate is 0.1 divided by 12

4. Continuous compounding

Special case

If m approaches infinity, then the compouding equation turns into

- The number e is a constant and equals approximately 2.1828.

- The number e is similar to pi and has not pattern in the number.

- Example

- You deposit $50 into your bank and forget about it for 70 years.

- The bank used continuous compounding, then your savings grow into:

- If you used monthly compounding, then your savings would be $9,373.90

|

Annuities and Mortgages

|

|

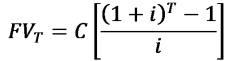

1. Annuity - an investment for people planning for retiring

- Annuities are two types

-

Ordinary Annuity

- Payment is due at the end of period

-

Annuity Due

- Payment is due at the beginning of the period

- We will stick to ordinary annuities

- Example - you are investing into an annuity

- Interest rate is 9% APR that is compounded annually

- You are investing in $20,000 per year for five years

- What is the Future Value of your annuity?

- Did you notice the exponents?

- A formula exist that calculates the future value of annuities

- Example

- You plan to retire and you want $40,000 ordinary annuity

- You will pay 4 annual payments at the end of the period

- The interest rate is 3%

- What are your annual payments?

All future payments are the same, so

2. Calculate a home mortgage. Start with the formula.

- All FV t are future mortgage payments

- r is interest rate (loan rate) and fixed throughout life of the loan.

- PV 0 is the bank loan, when you bought the house

All loan payments are the same, so FV = FV 1 = FV 2 = FV 3 = ... = FV t

Incorporate into the equation

- Example

- Mortgage: $60,000

- Interest rate: 12%

- Six-year loan

- Paid yearly

- Solving for FV, your payment yearly payment is $14,594.

- Build an

Amortization Table

. This table show the breakdown of interest and principal paid for each payment.

- Example

- At the end of Year 1, you have $60,000 outstanding.

- Your interest is 12% multiplied by $60,000, which is $7,200.

- Your payment is $14,594, so interest is $7,200, the remainder reduces the loan balance.

- Year 2, and beyond, repeat the sequence.

|

Payment |

Interest |

Principal Paid |

Loan Balance |

| Year 0 |

- |

- |

- |

$60,000 |

| Year 1 |

$14,594 |

$7,200 |

$7,394 |

$52,606 |

| Year 2 |

$14,594 |

$6,313 |

$8,281 |

$44,325 |

| Year 3 |

$14,594 |

$5,319 |

$9,275 |

$35,050 |

| Year 4 |

$14,594 |

$4,206 |

$10,388 |

$24,662 |

| Year 5 |

$14,594 |

$2,959 |

$11,635 |

$13,027 |

| Year 6 |

$14,594 |

$1,563 |

$13,027 |

$0 |

If you pay the mortgage monthly, divide interest rate by 12 and multiply the number of years by 12.

A 20 year mortgage will have 240 payments. I have a program that calculates the amortization table for long time periods.

The amortization table can also handle balloon payments and variable interest rate mortgages.

|

Comparing Different Investments

|

|

1.

Net Present Value (NPV)

- Calculate the net present value

- Change the present value equation into the form

- You paid out PV 0 for the investment

- Any FV's will be negative if it is a payout

- The return to the project is r

- Invest in the project with the highest NPV

- NPV has to equal or greater than zero

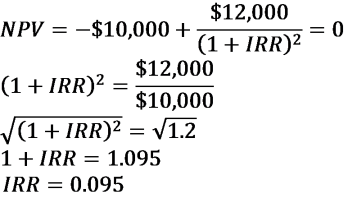

- Example

- Your brother wants you to invest $10,000 into his business

- He will promise you $12,000 in two years

- The projected rate of return is 10%

- You buy a T-bill for $9,000

- A year later, the U.S. gov. will pay back $10,000

- The projected rate of return is 4%

- Calculate the NPV's for both situations

Brother's business

T-bill investment

- Conclusion - invests in the T-bill

2.

Yield to Maturity

- set the Net Present Value to zero and solve for the return

- Also called

Internal Rate of Return (IRR)

- Use numerical techniques

- I have a program that uses two techniques

- Grid Search - try various r values until NPV equals zero

- Find the Root - an algorithm that finds roots to the equation

- Example:

- Your brother wants you to invest $10,000 into his business

- He will promise you $12,000 in two years

- You can invest in a CD that pays 3% APR

- If you trust your brother, then you earn a higher rate of return.

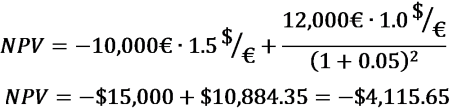

3. Foreign Currencies - more difficult to deal with

- Exchange rates are continuously changing

- We assume we know the exchange rate at every point in time

- Convert exchange rate to home currency

- Exchange rates are E 0, E 1, E 2, and E n

- Example

- You invest 10,000 euros into Greece

- You expect to earn 12,000 euros in two years

- Projected rate of return is 5%

- Exchange rate at time 0 is $1.5 per 1 euro

- Projected exchange rate in two years is $1.6 per 1 euro

- The NPV is

- Instead we had the Greek Financial Crisis

- In Year 2, the exchange rate decreases to $1 per 1 euro

- The NPV is:

- You were harmed by the depreciating Euro

4. Inflation - we can compute a real net present value and a nominal present value.

- Both results in the same number, because the inflation term falls out of the equation.

- Start with real FV and the real interest rate

- Convert the cash flow into nominal by substituting the Fisher Equation into the equation:

- Note - FV's are still in real, but are converted into nominal by multiplying it by expected inflation

|

Compounding Different Rates of Return

|

|

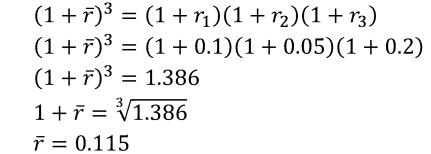

1. What do you do, if over the life of a project, you have different rates of return?

- Example 1

- Year 1, r 1 = 10%

- Year 2, r 2 = 5%

- Year 3, r 3=20%

- Calculating the rate of return is using the geometric average

- r bar is the average rate of return in annualized return

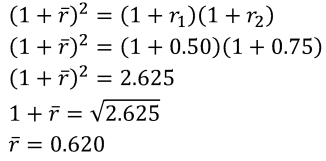

- Example 2

- Year 1, r 1 = 50%

- Year 2, r 2 = 75%

- Calculating the rate of return is using the geometric average

- r bar is the average rate of return in annualized return

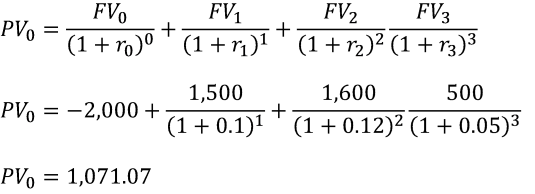

2. What is the present value of the following cash flows from a project with different returns for each year?

- You invest $2,000 today

- Year 1, you receive $1,500 with a 10% interest rate

- Year 2, you receive $1,600 with a 12% interest rate

- Year 3, you receive $500 with a 5% interest rate

- The net present value is:

|

You should only invest in a project, if the net present value is greater than zero. |

|